You’ve already done the hardest part of calculating if your retirement savings are on track: You’ve decided to actually do it and are STARTING the process. Honestly–getting your retirement savings on track isn’t rocket science, it’s just complicated enough that people get intimidated out of starting the process.

I’ve laid out a few options for you. If you use anyone other them,

You will have a retirement plan by the end of the day.

Option 1: Use Empower‘s awesome retirement planner (recommended) and FREE .

Option 2: Use a rule of thumb (go to rule of thumb)

Option 3: Use a retirement calculator (go to retirement calculator)

Honestly, the hardest thing about the whole process is digging up your investment account logins, but that’s something you need to do anyway! I promise–you’ll be SO GLAD you finally figured out how to get on track for retirement, you’ll want to break out a dance to celebrate making such a Money Fit Move.

Retirement Planning Can be Complicated

Planning for retirement can be complicated because it involves a lot of assumptions including:

- Your income (which changes)

- Your savings rate (and, conversely, your annual expenses)

- Inflation (most people assume between 3-3.5% for this but no one knows what inflation will be)

- Investment return rate (which no one knows for sure–for retirement planning, people often use 7%–not adjusted for inflation)

- How long we’ll live after retirement–We want a long life, but we also don’t want our money to run out. (Don’t freak out about this too much–retirement planners can help you figure out a Safe Withdrawal Rate to significantly lower the risk of running out of money during your lifetime).

And most retirement calculators don’t account for important one-time events such as:

- Buying/selling homes

- Selling a business or partnership interest

- Other significant income or expense events

There is one AMAZING retirement calculator . . .

Notice I said most retirement tools don’t take these things into account. There is one amazing retirement calculator that is powerful, easy to use, AND FREE! Honestly, it’s so superior to other retirement calculators I’ve found, they could charge for it and I would still recommend it over other retirement calculators. Maybe someday it won’t be free. But, for now, it is free and it’s amazing.

It’s the best Retirement Planning tool and it’s FREE? What’s the catch?

Empower also offers (cheaper-than-average) investment and wealth management services that they hope you will someday use.

Do you ever have to use Empower’s paid services? Nope.

Should you use them? We do. But we spent a few years falling in love with their free tools first. FYI – Empower’s Investment services become available when your portfolio reaches $100k-$200k, wealth management services are available when you have $200k+ in assets. But their FREE planning tools are available to anyone, anytime.

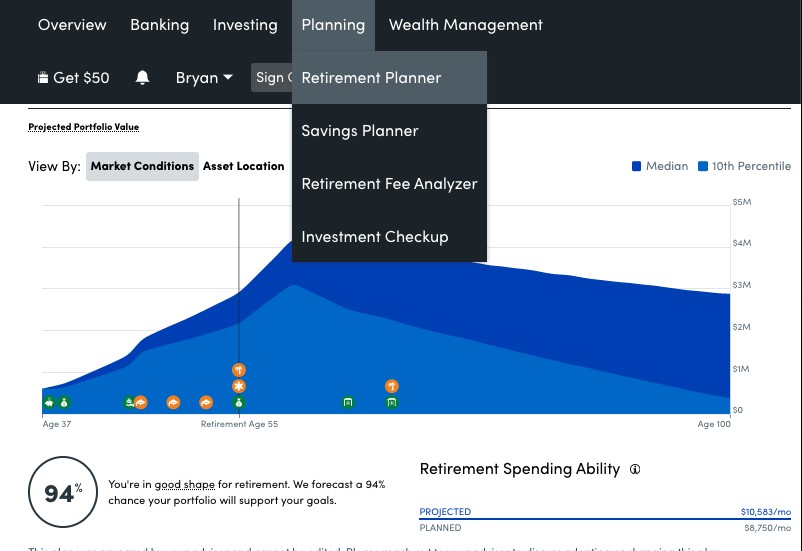

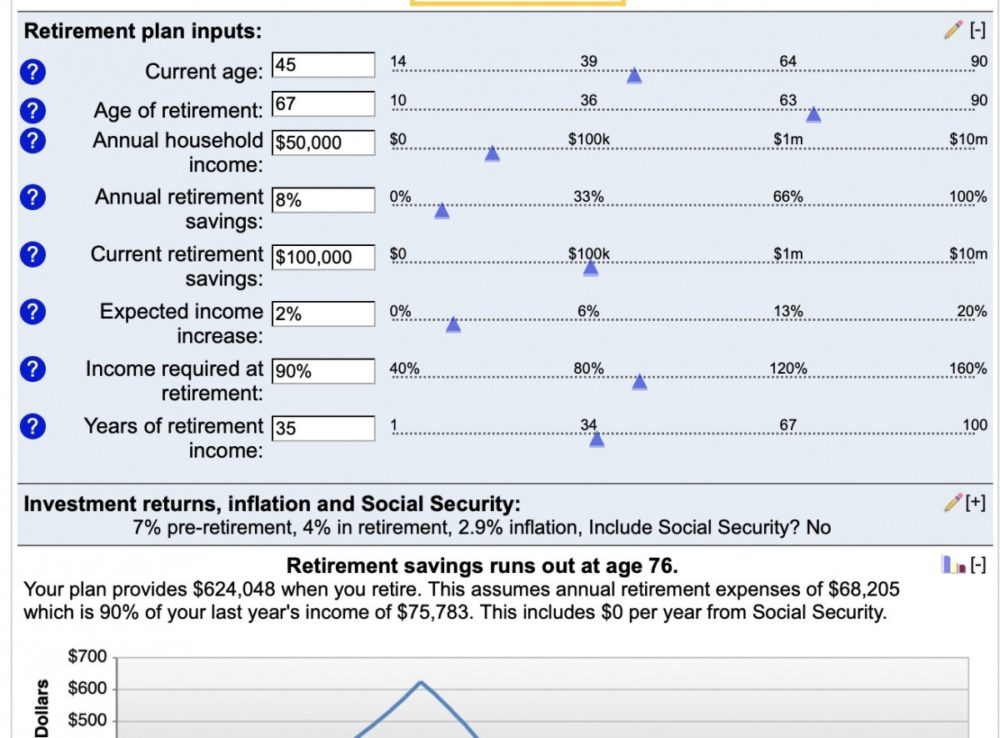

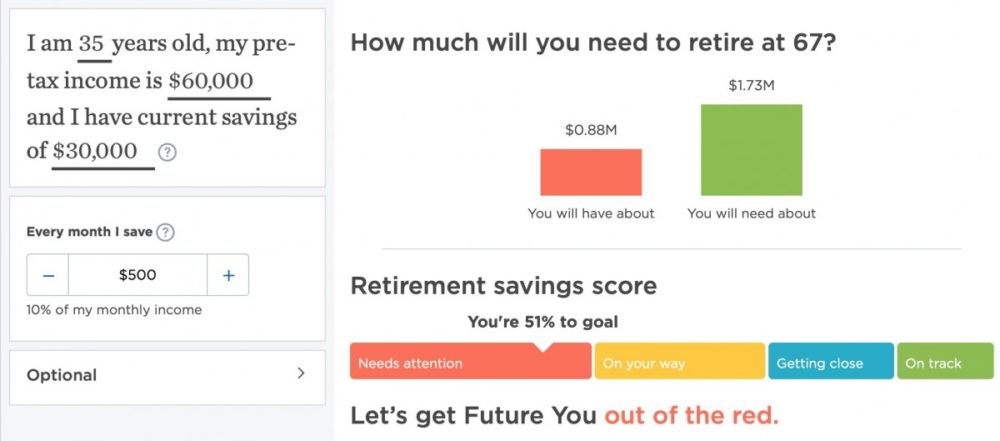

OPTION 1: BEST (free!) Retirement Planning Tool: EMPOWER (affiliate link)

The best retirement planning tool I’ve come across is–by far–Empower.

Their retirement calculator takes into account:

- Savings rate

- Social Security (optional)

- The current value and allocation of investment/retirement accounts

- One-time events (EMPOWER IS THE ONLY CALCULATOR I’VE FOUND THAT DOES THIS!!):

- e.g. Buying/Selling a home

- Any other income/expenses streams or events

- Planned Spending. You can guess on this (although it’s helpful if you keep a budget).

- If you’re unsure how much you spend, you have the option to link/ import your bank and credit card accounts and Empower will track your spending for you.

- I recommend YNAB for your budgeting/cash flow tracking needs, but if you love having things all in one place, Empower also has a savings tracker.

- If you’re unsure how much you spend, you have the option to link/ import your bank and credit card accounts and Empower will track your spending for you.

3 Steps: How to Use Empower’s FREE Retirement Planner (plus other free financial tools)

Step 1: Create a FREE account with Empower

Calculate your NET WORTH. Get your FREE, secure Financial Dashboard (Affiliate Link)

Step 2: Connect and Sync Accounts

Empower is sort of the “Mint” of investing. The financial software allows you to pull in all your investment/bank accounts from all over into one handy dashboard. Watch your financial dreams become reality as you can then chart your overall progress towards your financial goals, such as retirement.

You can use the dashboard for free without having to enroll as a client of Empower’s wealth management and investment services. If you’re not interested in Empower’s wealth management services, tell them as much and they will leave you alone. Personally, we do use Empower’s wealth management services. We’re happy with the results of our portfolio and the strategic decisions PC makes to maximize tax benefits. But we happily used their free software for years before deciding to use their paid services.

Step 3: Click on Planning: Retirement Planner

Edit the Income Events and Spending Goals to figure out how likely you are to get on have the retirement of your dreams.

Questions/Comments about Empower

My husband and I have happily used Empower since 2016. We actually had a little tiff today fighting for credit over who discovered them (just so you know–I discovered Empower, but I delegated to my husband to go through the actual sign-up process, so I’ll share credit). 😉

If you have any questions about Empower, feel free to reach out to me via Facebook, Instagram or Pinterest.

OPTION 2: Use a Retirement Planning Rule of Thumb

It’s not as robust or precise, but it works for post-it note ballpark planning.

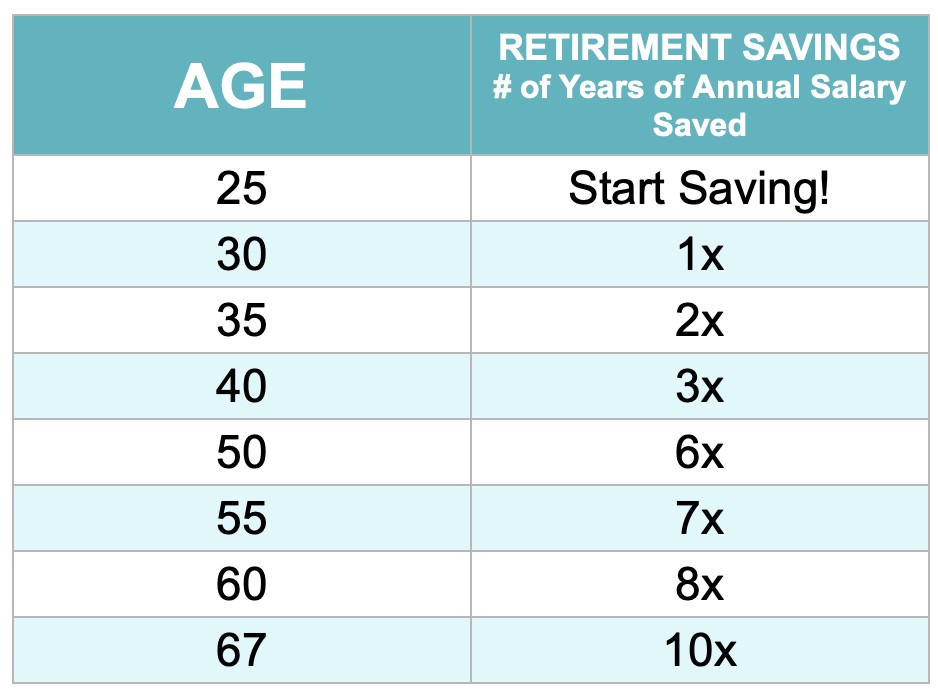

RULE OF THUMB #1: Fidelity’s 10x Income Approach to Retiring by Age 67

Fidelity’s Recommendation: If you want to Retire by Age 67: Have 10 Times your final salary in retirement savings.

Fidelity, who helps a lot of people manage their retirement savings, did some research about retirement savings goals. Their recommended rule-of-thumb for people who want to retire by age 67 is to save 10x of your current salary. Obviously, your salary will change over the years–that’s part of the point. That way, your retirement savings will track to inflation and–most likely–your spending.

Milestones

Fidelity’s Assumption: If you retire with 10x your final salary at age 67, these savings will provide 45% of your pretax, preretirement income.

Example:

So if your final salary is $100,000, by age 67, you should have x 10 saved $1,000,000 for retirement. This will allow you to live on $45,000 a year from your retirement savings ($150,000 x 45%) with the rest from any social security you get. The exact amount that you can live on will generally depend on your income, retirement age, and other factors such a portfolio performance.

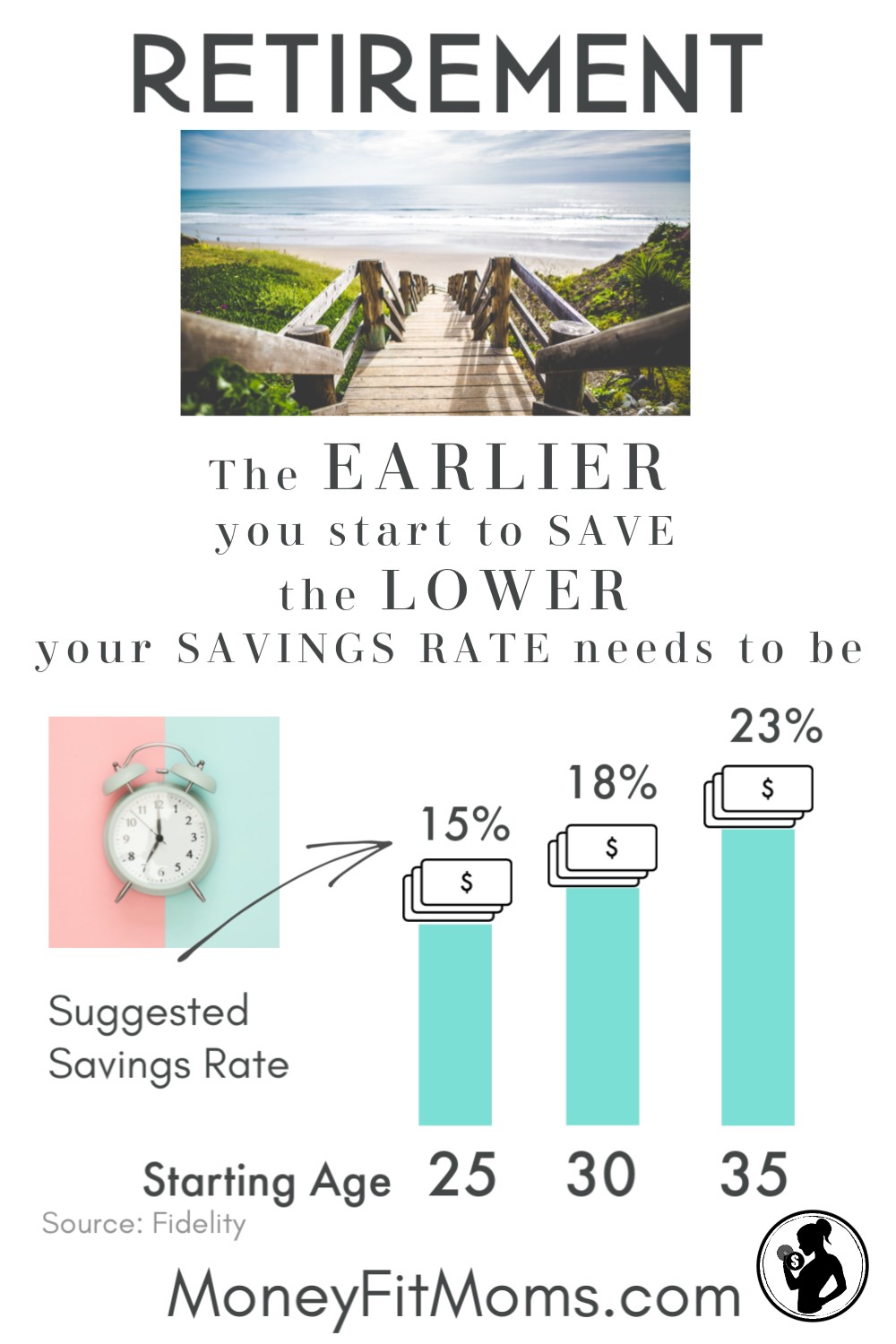

How Much Do I Need to Save to hit 10x Income Savings at Retirement?

It depends on when you start. The earlier you start, the lower your savings rate can be:

What if you don’t have 10x Income at retirement?

The “safe withdrawal rate” is generally considered to be 4% of your investment portfolio. So if you have $1,000,000 in retirement savings, you can live off of $40,000 a year. This assumes a 7% return and a 3% rate of inflation. Neither investment returns or inflation are guaranteed, so you might need to adjust your spending in a recession.

Limitations of the 10x Income Approach

This calculation has its limitations if, for example, you live on significantly less than your salary. Some people, such as this writer at Forbes, think these goals are being overly conservative and, if you get Social Security on top of this, you will be somewhat over-saving. But I would much rather err on the side of over-saving than under-saving. Not having enough money to retire would be awful, but realizing I have enough money to spoil my grandkids and travel extensively seems like a pretty sweet problem to have.

What if I want to retire early?

Depending on the standard of living you want to have, Fidelity recommends you save been 11x-16x your current salary.

Try Fidelity’s 10x Income Savings Calculator

OPTION 2: RULE OF THUMB: FIRE (Early Retirement)

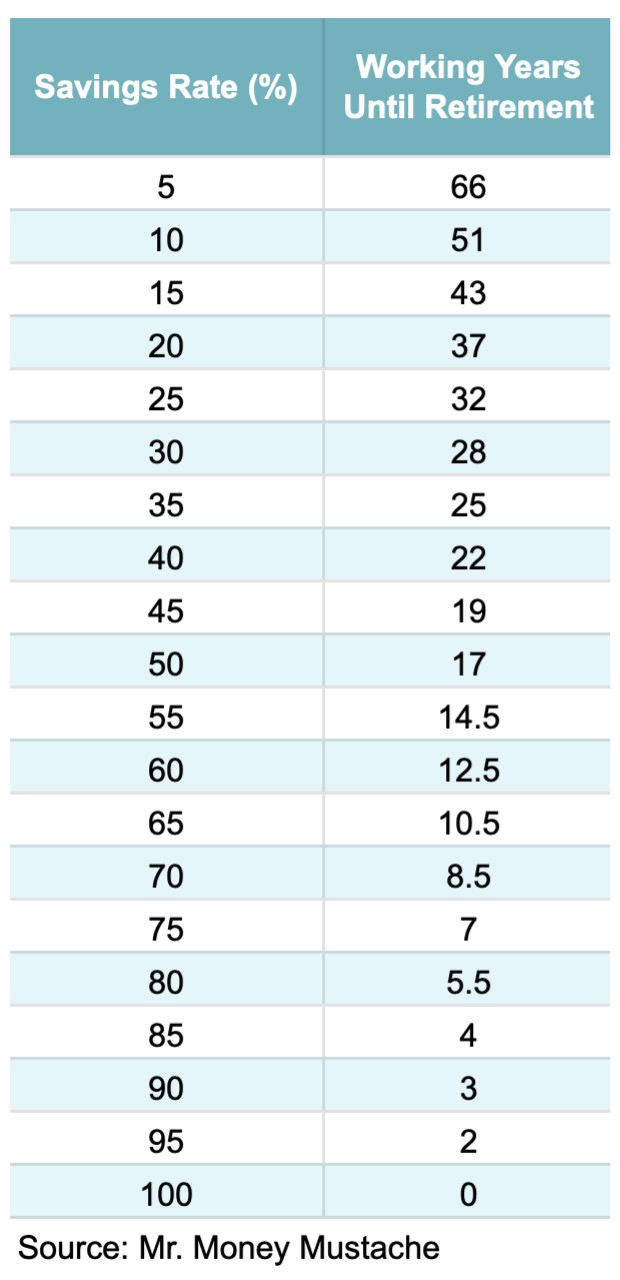

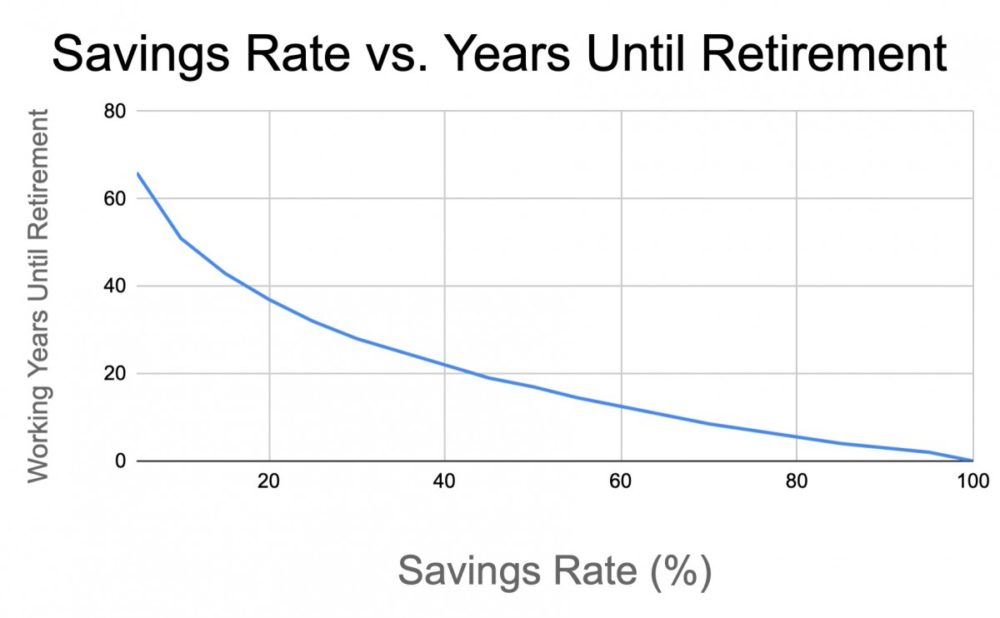

Mr. Money Mustache – Savings Rate Percentage vs. Years Until Retirement

Helpful if you’re trying to RETIRE EARLY.

Mr. Money Mustache swears by the calculation that your Savings Rate Percentage (of your take-home pay) directly calculates the number of working years until retirement. Check out this article if you’re trying to build a FatFIRE (high expense early retirement).

His assumptions:

- 5% investment returns (after inflation–not the most conservative estimate, but also not unreasonable considering historical long-term investment returns)

- That you can live off a 4% withdrawal rate after retirement (adjusting your spending as needed during recessions). This is called your Safe Withdrawal Rate, so you don’t run out of money in your lifetime.

- Meaning: if at retirement your nest egg is $1,000,000 x 4% = $40,000 = amount you can spend for living expenses each year / 12 = $3,333 per month.

- This way, you’ll only be touching the gains. If your investments grow at 5% and you only take 4%, this leaves a safety margin. By this logic, this investment portfolio income will last you as long as needed–even 70+ years if you retire at age 30 and live to be 100.

According to his calculations, this is the correlation between savings rate and working years until retirement.

Note: This is assuming you have a starting net retirement savings of ZERO (meaning NO savings).

If you have a starting balance you want to include in your calculation, try one of the calculators above, or use the most dynamic Retirement Calculator by creating an account with Empower.

Take-Home Pay

Amount of your paycheck that actually went into your bank account

+ any retirement contributions subtracted from your paycheck (check your paystub)

Take-Home Pay (for this calculation anyway)

For Example:

Gross salary: $100,000 / 26 pay periods = $3,846 per pay period

After your employer takes out taxes, 401k contributions, health insurance benefits, etc., let’s say your net pay is around $69,480.

401k contributions: 5% from you ($5,000) + another 2% from your employer ($2,000) = $7,000 annual retirement savings/contributions

+ Add back your 401k contributions to figure out your take-home pay.

Annual Take-Home Pay: $69,480 = Annual Net Pay + $5,000 401(k) contributions add-back

Annual Savings Percentage: 10% – See Chart: 51 years more working years until retirement. If you’re 25 when you start saving this much for retirement, you would be on track to retire around age 75.

$7,000 (retirement savings/contributions) / $69,480 (net take-home pay) = 10%

Yikes! Let’s bump up those retirement savings.

If you’re already contributing enough to max out your employer’s 401k contributions, your next best option would probably be contributing to a Roth IRA (assuming you’re under the income limitations).

The Roth contribution limit for 2020 is $6,000. That’s $500 per month. Let’s say you scrimp and save to make it happen–you open an IRA and start contributing.

YOUR NEW SAVINGS Percentage: 18.7% – Check Chart: That puts you between the 15-20% Mark – 37 – 43 years until retirement, closer to 37 years.

et’s assume 39 years until retirement + If you’re age 25 = Age 64.

$5,000 (your 401k contribution + $2,000 (your employers 401k match) + $6,000 (Roth Contribution) = $13,000 annual retirement savings/contributions / $69,480 (take-home pay) = 18.7%

You are looking good for an on-time retirement! If you get social security or any other income streams, that’ll just be the cherry on top.

Limitations of This Calculation

Because MMM’s calculation assumes a constant savings and expenses rate, these calculations don’t work out for people with large one-time events like selling a business/home. This is why I so vehemently recommend the Empower Retirement Calculator.

Saving Rate is the KEY to Retirement

Despite its limitations, this calculation does accomplish its purpose: to fire you up to increase your SAVINGS RATE = the KEY to retirement.

It makes sense when you think about it:

If you’re not saving anything: you won’t technically ever be able to retire, unless there is something left in the nation’s social security fund (pro tip: this is dangerous–DO NOT rely on social security and you won’t be disappointed).

On the other hand, if your expenses are always zero, then your savings rate is 100%: You can retire anytime because you don’t have any expenses to cover.

OPTION 3: Simple Retirement CALCULATORS (Not as dynamic as Empower)

If you want a super simple retirement calculator, here are a few options (once again–these only let you figure out steady-line income/expenses scenarios):

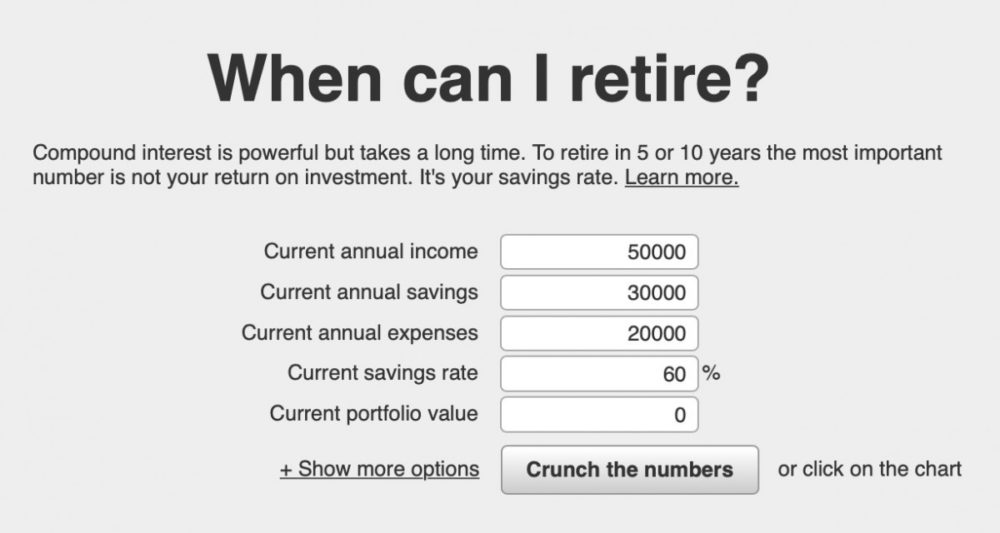

Networthify – Early Retirement Calculator – My favorite part about this calculator is it emphasizes that your SAVINGS RATE is the most important factor in determining when you can retire.

Bankrate Retirement Calculator: Calculates how long your retirement savings will last.

NerdWallet Retirement Calculator: How much money will you need to retire?

Winner: Empower

In summary, these other calculations are great for getting a basic idea of where you are and where you need to be. But if you want a free retirement planner, that you will keep using to run new scenarios, create a free account with Empower.

Calculate your NET WORTH. Get your FREE, secure Financial Dashboard (Affiliate Link)

Expect Peaks and Valley along the Way

Remember that you’re in this for the long-haul. Retirement savings will increase and dip with market fluctuations. As long as you’re diversified or using index funds, you can ride those waves. Resist the urge to try to time the market! You’ll end up doing what all scared investors do: buying high and selling low–the exact OPPOSITE of what you want to do.

You set up a plan for retirement–Now CELEBRATE!

Aren’t you glad you figured out how to get on track for retirement? Even if you’re not happy with where you are right now in your progress toward retirement, now you can work towards where you want to be! With some hard work, you’ll be on track for the retirement of your dreams.

Sources:

Empower

Fidelity – How Much Money Should I Save

TheBalance.com – Retirement Savings Benchmarks

Financial-Planning.com – A Magic Formula for Retirement Planning

NerdWallet.com – Do the Math to Tell if You’re on Track for Retirement

Mr. Money Mustache – The Shockingly Simple Math Behind Early Retirement

Mr. Money Mustache – The Race to Retirement – Revisited

Forbes – How Much Should I Have Saved Toward Retirement

Empower Personal Wealth, LLC (“EPW”) compensates Money Fit LLC for new leads. Money Fit LLC is not an investment client of Empower Advisory Group, LLC.