Why is a fully-funded emergency fund the secret to building wealth? Not only will it protect you from going into costly debt, but it will also allow you to INVEST with confidence. Long-Term Investing is an effective way to build wealth (e.g. with tax-advantaged investment accounts). But very few people are maxing out their retirement contributions! They stop at the free employer match (so glad they’re not missing out on that free money). But what makes people hesitate to invest MORE? They are worried they might need that money later. And they’re right! But that’s where an EMERGENCY FUND comes in. Having an emergency fund with 3-6 months’ worth of expenses will protect your assets from life’s inevitable downturns and keep your financial goals on track, allowing you to INVEST with CONFIDENCE.

An emergency fund is ESSENTIAL–the type of “insurance” that nobody thinks about but everyone needs. I can’t predict the future, but I can tell you one thing: Life WILL happen to you. You WILL have large, unexpected expenses.

That’s why building your emergency fund is step 4 of my FREE Money Fit Challenge.

Improve your BUDGETING & INVESTING! Join the FREE #MoneyFitChallenge

What is an emergency fund?

3-6 months of expenses saved in case of large, unexpected expenses, such as:

- Health issues (the number one cause of bankruptcy–both from medical bills but also the loss of income from unexpected health issues, disability, and death)

- Job loss

- Unexpected car or house repair (e.g your roof fails earlier than planner)

- Another emergency.

Why have an Emergency Fund?

It’s important to have some cash set aside that is dedicated to getting you through those inevitable “rainy days.”

People with a home and large retirement accounts sometimes feel safe against hard times, but as you know, you can’t eat a house.

The only way that a house or retirement can provide you with financial security against emergencies if you liquidate them aka turn them to cash by:

(1) Selling your house or taking out a home equity loan (You do NOT want to do this!)

(2) Take an “early” or “premature” distribution from your retirement account, often incurring penalties–making those distributions EXPENSIVE, especially when you consider the growth you’re missing out by not letting that money grow. Investments grow the most in their last years. (We don’t want this either!)

So think of an emergency fund as insurance to protect your home, investments, and other assets. That way, you don’t have to cover a large unexpected expense by dipping into your retirement or investments.

“But cash loses value! That money could be used somewhere else.”

That is true, but . . . emergency funds are not supposed to be making you money. It’s INSURANCE. Insurance costs money. Plus, an emergency fund will allow you to put money where it will REALLY grow: Long-Term Investing.

Should I put it into a money market or other interest-bearing account?

Sure. But FYI:

- A good savings accounts sometimes earn more than money market accounts.

- Savings accounts often have more flexibility/liquidity than money market accounts and the interest in any kind of liquid account will usually be minimal in most markets anyway.

- Many money market and similar accounts have penalties for dropping below a certain minimum balance.

The account you keep your emergency fund in should be able to be immediately liquidated (aka cashed out) without incurring penalties. I wouldn’t recommend opening a new bank account just to chase what a certain money market account is currently offering.

A BETTER option than stressing over the highest-interest place to put your Emergency Fund:

Budgeting and cash management. Meaning: If you’re actively managing the amount your set aside for upcoming expenses, emergency fund, etc. than you can be confident about leaving some money in cash and INVESTING the rest.

What do I mean about this? You’re better off leaving the “just-right” amount in cash and investing the rest than to keep TOO much cash because you feel good about the fact that it’s in a low-interest earning money market account. INVESTING is where you’re going to grow your money. An EMERGENCY FUND is a costly but critical insurance.

“But it will take me so long to save for an Emergency Fund!”

You won’t have to save for your emergency fund forever. Once it’s fully funded, you can go back to packing away your excess income in investments and other financial goals.

You won’t have to contribute to your emergency fund again until:

(1) You use it for an emergency and need to re-build it (at which point you will be SO glad you had one rather than being stressed and/or having to liquidate your house/investment accounts/or other assets.

or

(2) Your target fund balances changes due to:

- An increase in your income or monthly burn rate (expenses)

- Your risk changes so you feel like you need more months’ worth of expenses covered (e.g. Your health changes or you switch to a less-secure or harder-to-replace job)

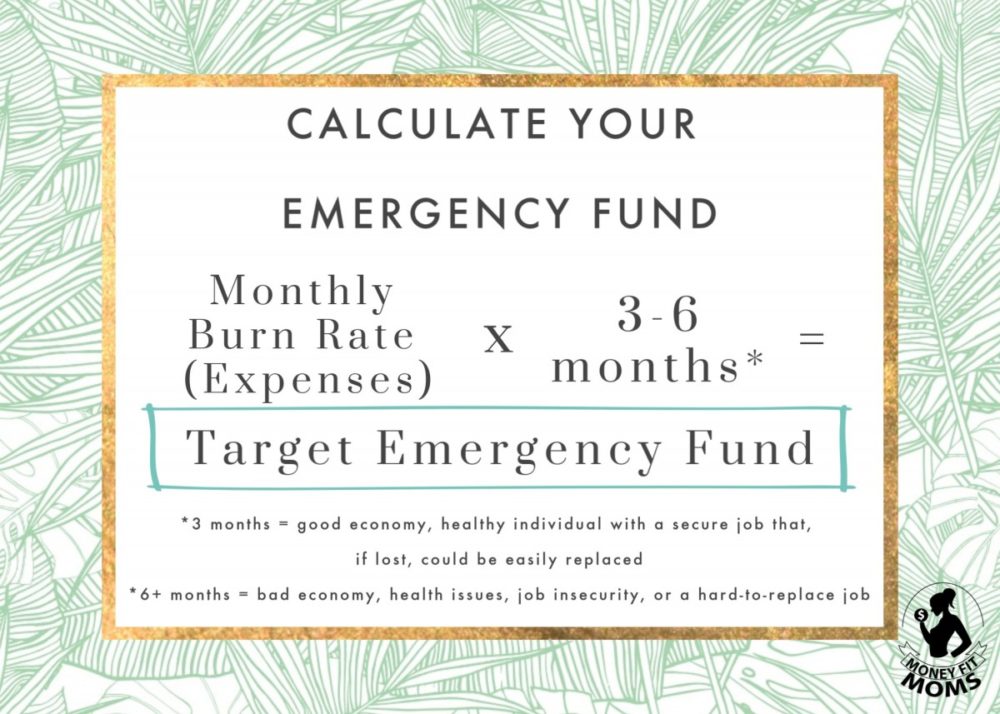

HOW MUCH should you save for your Emergency Fund?

How to calculate your MONTHLY BURN RATE

– Your monthly expenses, either estimated or — preferably — based on your budget. You have to imagine how much you’d spend each month in an emergency situation. You might be able to cut out some discretionary expenses, but you’re also likely to have some additional expenses in an emergency situation such as medical bills.

How many months should you have?

Between 3 to 6 months, but exactly how many months depends on your:

- personal situation and

- risk tolerance.

Basically, the higher the risk your job/health/financial situation is, the more months you should have saved.

You can ask yourself questions like:

- How are the economy and job market?

- Am I likely to lose my job?

- How long would it take me or my partner to get a new job?

- Am I healthy?

- What is my personal risk tolerance? How many months would make me feel comfortable?

- How many months do I want to be able to live without a paycheck?

Where should I save my emergency fund?

“Do I need to open a separate account for my emergency fund?”

It’s a good idea. Or if you’re a super disciplined budgeter (or use a really great budgeting tool like YNAB), you could designate a certain amount of your savings account as your “emergency fund.”

Example:

Let’s say your monthly burn rate is $5,000 and your risk/job makes you want to keep 3 months worth of expenses in your emergency fund:

$5,000 x 3 months = $15,000 Target Emergency Fund

So you might:

- Open a separate account for your emergency fund so you’re not tempted to spend it

-OR-

- If you’re a super-disciplined budgeter: Designate the first $15,000 (or whatever your target) of your savings account as your emergency fund–not to be touched. Anything above that is general savings. If your balance ever drops before $15,000, you know that you’ve dipped into your fund and it’s time to rebuild.

What does NOT constitute an emergency?

Planned expenses. This isn’t how you save for a new car or house project–that should be a SEPARATE SAVINGS goal. An emergency is, by definition, an unexpected, unplanned event.

Do people actually use their emergency funds?

We’ve used ours twice, both for health-related events. I had severe postpartum health issues (postpartum anxiety and insomnia) that resulted in thousands of dollars in medical bills. Other than spending our emergency fund, we’ve also re-evaluated and re-built it multiple times based on changes in monthly expenses and job security.

Emergency Fund Calculator

Check out this calculator:

The Takeaway

Building an Emergency Fund is Step 4 of the FREE Money Fit Challenge!

Join the supportive @MoneyFitMoves Community! We’re onInstagram, Facebook and Pinterest, YouTube, and TikTok.

More ABOUT ME